Fusion met 'AI power' — and became a real business

Here's the deal: fusion has always been "the technology that's 30 years away." Then on June 4, a deal landed that makes the joke look stale. Sam Altman-backed fusion startup Helion said it closed a $465 million Series G at a $15.5 billion valuation, bringing total funding to $1.5 billion.

More telling than the numbers is "why now, at this price." Helion was valued at roughly $5.43 billion in January 2025 — nearly tripled in 18 months. In a field that hasn't sold a single watt of commercial electricity, a jump like that has one explanation: the explosive power demand of AI data centers. Helion is the first fusion company to commit to supplying power to Microsoft, and this round funds the very plant that will do it.

Thrive Capital led the round. New investors include Alta Park Capital, Anti Fund, BoxGroup, Lux Capital, Peak XV Partners, and Ford Executive Chairman Bill Ford; existing backers Lightspeed, SoftBank Vision Fund 2, and Dustin Moskovitz (via Good Ventures) re-upped. The crux: capital recognized — early — the moment fusion gets reclassified from "science project" to "power infrastructure for the AI era."

The players — Helion, Sam Altman, and Microsoft

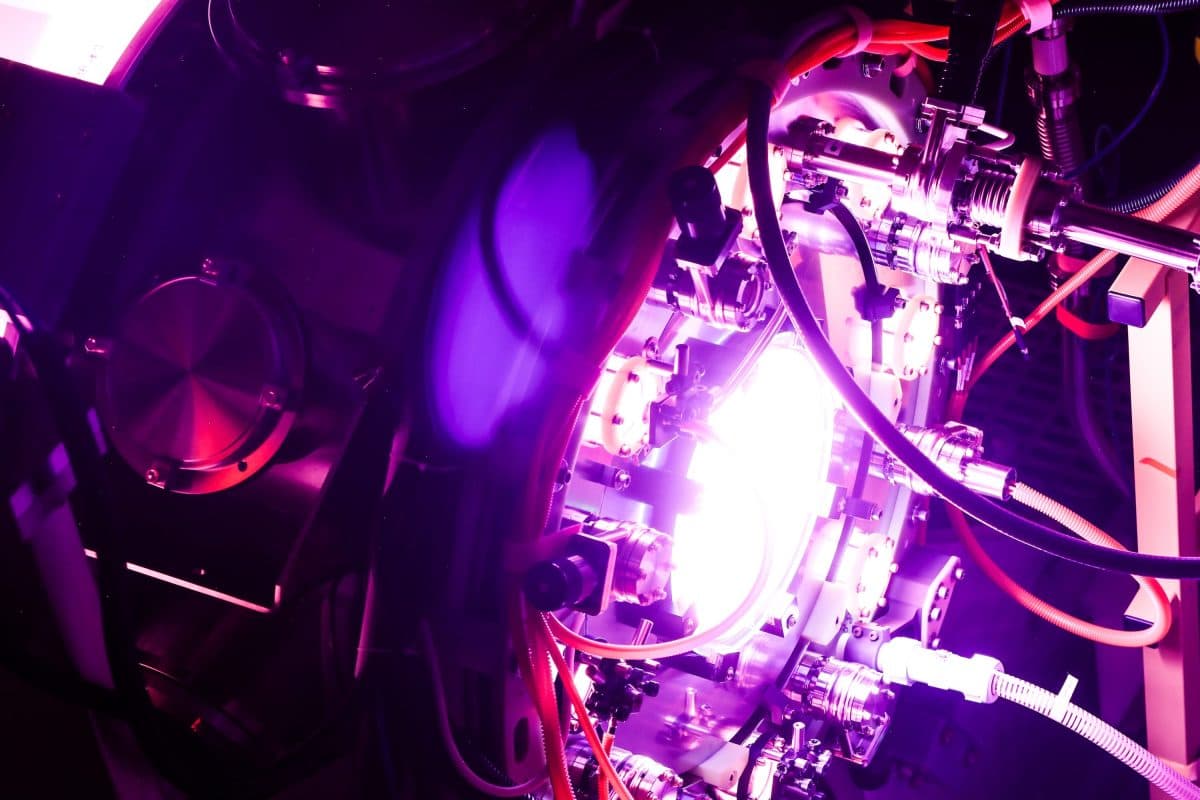

First, Helion. A fusion energy company in Washington state. Unlike most fusion startups chasing giant tokamaks (donut-shaped magnetic devices), Helion uses a different "magneto-inertial" approach and extracts electricity directly from the fusion reaction — skipping the steam turbine. It's a bet on faster, smaller, cheaper. Its 7th-generation Polaris prototype hit industry firsts: the first privately funded fusion machine to operate with deuterium-tritium (D-T) fuel, and it broke its own record by pushing plasma temperatures past 150 million °C.

Next, Sam Altman. Famous as OpenAI's CEO, he's also Helion's chairman and key backer. That creates an odd symmetry — the OpenAI he runs operates some of the world's most power-hungry AI, while the Helion he backs builds the fusion to feed it. His worldview ("scaling AI needs power; making power needs fusion") interlocks inside one person.

The last player is Microsoft. Helion signed "the world's first fusion power purchase agreement (PPA)" with Microsoft back in 2023. Microsoft agreed to buy electricity from Helion's first plant — Orion, a ~50 MW facility in Malaga, Washington — targeting operation in 2028. So this isn't a vague vision; it's a plant with a buyer already lined up, which is exactly why investors leaned in.

What's inside — the numbers and the contract

The core figures, side by side:

| Metric | This round | Prior (Jan 2025) |

|---|---|---|

| Round size | $465M (Series G) | — |

| Valuation | $15.5B | ~$5.43B |

| Total funding | $1.5B | — |

| Lead investor | Thrive Capital | — |

| First plant | Orion (~50 MW, Malaga WA, 2028 target) | — |

| Offtake customer | Microsoft (world's first fusion PPA) | — |

The standout is the ~3x valuation jump in 18 months. Fusion is capital-intensive and far from commercialization, so valuations usually move slowly — Helion broke that norm. Two reasons: (1) meaningful technical progress on the Polaris prototype, and (2) "AI power" demand instantly raising fusion's business case. Investors started seeing "infrastructure that gets paid soon," not "distant-future science."

The second point is use of proceeds. The $465M goes clearly to three things: (1) accelerating commercial fusion deployment, (2) scaling manufacturing, and (3) expanding the ability to deliver clean power to customers. Building Orion is central — this is the money that bridges a lab prototype to a plant that actually sells electricity.

The third is the investor mix. Thrive Capital leading matters — Thrive is also a deep OpenAI backer, so within the "Altman ecosystem" you see a combined bet on AI and power. Adding Bill Ford (autos), SoftBank's Vision Fund, and Lux Capital (deep tech) — capital of very different stripes — signals that fusion is now viewed not as a single-sector bet but as infrastructure many industries jointly need.

Who wins — Helion, Microsoft, and the AI industry

For Helion, the raise buys runway and credibility at once. Building a fusion plant takes astronomical capital, and this round speeds up Orion's construction. More importantly, a $15.5B valuation and a top-tier investor list are themselves certification that "Helion is a serious contender" — an advantage in hiring, securing supply chains, and navigating regulators.

For Microsoft, it's securing AI-era power early. AI data centers need round-the-clock, stable electricity; solar and wind are intermittent and nuclear fission takes a decade-plus to build. If Helion delivers carbon-free fusion power by 2028 as promised, Microsoft locks in "clean, stable, large-scale power" before rivals. Even if the timeline slips, simply holding the PPA carries option value.

For the whole AI industry, it reveals where the bottleneck's center of gravity has moved. For years the AI race bottlenecked on GPUs; now power sits above that. Build more data centers and they're useless without electricity to plug in. Helion's round signals that capital markets have settled on the view that "scaling AI ultimately requires new power sources." It's one scene in a broader rush into fusion, advanced nuclear, and geothermal.

Past parallels — the promise and shadow of fusion bets

Capital betting on fusion isn't new. History gives a balanced lesson.

Grounds for optimism — private fusion accelerating. Over recent years, private players like Commonwealth Fusion Systems, TAE, and Helion have hit milestones faster than government-led ITER. The 2022 scientific ignition at the US National Ignition Facility (NIF) — getting out more energy than was put in — blunted the "fusion is impossible" skepticism. Helion's D-T operation and 150-million-degree result extend that progress.

A cautionary case — a field where "soon" keeps slipping. At the same time, fusion has a long history of repeatedly delayed "commercialization is imminent" promises. Between briefly making plasma and reliably sending power to the grid 24/7 lies a vast engineering valley. Helion's 2028 target is ambitious, but slipping timelines is closer to the rule than the exception in fusion. Remember, the 3x valuation prices in a "success scenario" in advance.

Two sides of capital — fast valuations, fast corrections. Valuations lifted by the AI theme can wobble first when the theme cools. Helion's value rests on assumptions that "Orion works on time and the Microsoft contract turns into real revenue." Shake those and $15.5B gets re-rated. Strong momentum is a double-edged sword.

Competitor counter-plays — other fusion, fission, and the grid

First, other fusion startups (Commonwealth Fusion, TAE, etc.). With Helion locking up "an AI big-tech customer plus a large round," rivals must find similar cards. In fact, big tech is spreading bets across fusion — buying options on multiple approaches rather than wagering on one. Helion's edge is its simple direct-electricity conversion and fast iteration; rivals can counter with "more validated tokamak physics" or "larger output."

Advanced fission (SMRs) is a formidable alternative. While fusion fields doubt about "will it really happen by 2028," small modular reactors win big-tech power contracts on the reassurance of "proven fission technology." Microsoft, Google, and Amazon all have nuclear bets laid down too. So Helion's real competition isn't only other fusion — it's every carbon-free power source that can switch on sooner.

The existing grid and natural gas are the pragmatic fallback you can't ignore. If plants aren't ready in time, data centers will lean on gas or the existing grid — even if that clashes with carbon targets. Helion's value proposition is "clean and reliable" at once; whether it truly delivers both is the crux of every rivalry. Fail, and the market drifts toward "less clean but certain."

So what actually changes — by persona

If you watch energy or infrastructure, this is a clear signal that AI power demand is reshaping capital flows in the energy industry. A structure where big tech prepays future plants via PPAs is taking hold. Carbon-free baseload — fusion, SMRs, geothermal — will be a hot capital-markets theme for years.

If you work in AI or are a founder, the key is that your model's limit may be power, not GPUs. If you're planning large-scale training or inference, "where you reliably get the electricity to plug your compute into" is an increasingly decisive variable, alongside securing the compute itself. Data-center siting, power contracts, and energy efficiency are starting to govern cost structures.

If you watch investment or industry trends, Helion's $15.5B symbolizes that AI and energy have become one body. One side (Flourish) makes AI use less power; the other (Helion) makes power cleaner and more abundant — and the two bets landed the same day, aimed at the same problem: AI's power crisis. Going forward, watch "the power to run it" as closely as "model performance."

Numbers and figures are as of announcement and may change. Investment calls are yours to make!

🥄 Three Things You're Probably Wondering

— Is Helion selling electricity now? No. It hasn't sold commercial power to the grid yet. It has hit technical milestones with the 7th-gen Polaris prototype, and its first commercial plant, Orion, is entering construction with a 2028 operation target. So the $15.5B valuation prices in "soon-to-be revenue," not current revenue.

— Why did Microsoft agree to buy fusion power? AI data centers need round-the-clock, carbon-free electricity, and few such sources exist in reality. If fusion works as promised, it satisfies three conditions at once: clean, reliable, and large-scale. By locking in the PPA first, Microsoft secures a future-power option even if the timeline slips.

— 3x valuation in 18 months — isn't that a bubble? A fair doubt. Fast valuation jumps are evidence of strong expectations and the thing most likely to wobble when they cool. Helion's value leans on "Orion works on time and the contract turns into revenue." Break those and it gets re-rated. That said, with real AI power demand underneath, it's a different flavor than a pure theme bubble.

— What does this mean for a regular person? Long term, it could affect electricity prices and carbon. As AI explodes power demand, commercializing carbon-free baseload like fusion would reshape the supply picture. You won't feel it immediately, but "where the AI era's electricity comes from" ultimately connects to everyone's power bills and environment.

References

- Helion Raises $465 Million Series G Funding Round to Meet Surging Global Demand for Power — Helion Energy

- Helion, the Sam Altman-backed fusion startup, raises $465M to build a power plant for Microsoft — TechCrunch

- Fusion Developer Helion Raises $465 Million at Triple its Prior Valuation — ESG Today

- Helion Raises $465 Million Series G Funding Round — BusinessWire

- Helion Energy — Official Site