In Half a Year, Korea Blew Past All of Last Year — But Only Some Founders Are Smiling

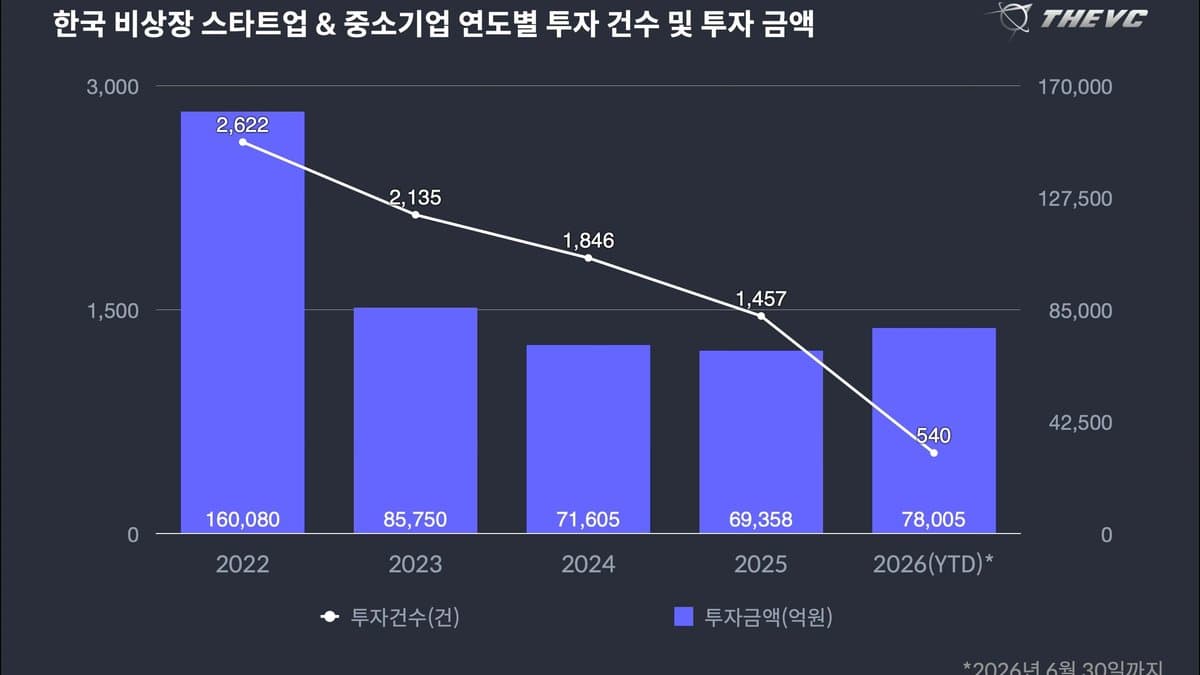

Here's the deal: on July 2, startup-data outfit THE VC dropped its Q2 2026 stats on Korean startup funding, and the headline number is genuinely big. Cumulative first-half investment hit ₩7.8005 trillion. All of last year came to ₩6.9358 trillion — and this year cleared that in six months. Against the same period last year, the dollar amount is up 204.7%. Not a gentle recovery. More than a tripling.

But if you stop right there and go "wow, Korean startups are booming," you've seen half the picture. In the exact same dataset, deal count actually dropped 5.4% year-over-year. Money tripled, but the number of deals shrank? That means the cash piled into a small number of huge rounds. In H1 there were 141 mega-deals of ₩10 billion or more, and those alone ate 93% of all the capital. The other several hundred startups split the remaining 7%.

And where did that money go? Overwhelmingly to AI and robotics. H1 AI/robotics investment alone hit ₩2.685 trillion, a 485.2% year-over-year explosion — more than double the pace of the overall market's 204.7% growth. At the seed stage specifically, 91.5% of the money went to AI and robotics. Basically, nine out of ten companies getting seed checks are wearing an AI badge.

So this number is good news ("Korea's venture market came roaring back") and scary news ("welcome to the era where it's AI or nothing") at the same time. Boom, concentration, or a narrowing bubble? Today we're cracking open that ₩7.8T figure to see who's actually laughing and who's crying.

First, Who Is THE VC Behind These Numbers

Let's get straight on what THE VC even is. Not a government agency, not a VC fund. It's a private data company that scrapes and organizes Korean startup investment history into a database. It tracks which company raised how much from whom and when — pulling from filings, press, and corporate records — then publishes quarterly and annual stats. It's one of the gauges venture folks reflexively check to take the market's temperature.

One thing matters here. THE VC's numbers use slightly different criteria from the government's official "venture investment" tally. Figures from the SME ministry or the Korea Venture Capital Association tend to only capture money flowing through registered venture funds, whereas THE VC tracks startup funding more broadly. So its numbers can run larger, and things like secondary share purchases get swept in too. Part of why this H1 figure looks so outsized is that counting method — keep that in mind.

Case in point: this ₩7.8T includes one deal that single-handedly reshapes the picture. Dunamu's ₩2.216 trillion secondary share acquisition. That one transaction accounts for more than a quarter of the entire half-year total. It's a bit different in character, since it's not fresh capital going into a startup via new shares — it's buying out existing shareholders' stakes. So THE VC also broke out a number excluding that secondary deal, and even then H1 came to ₩5.5692 trillion, roughly double the same period last year. In other words, yes, the market genuinely surged even without Dunamu. But if you take "₩7.8T" at face value you'll overstate things, so you need this context to read it right.

The other main characters are the ones receiving the money — AI and deep-tech startups. On the other side are the ones pushed out of this flow: founders in B2C services, commerce, and content, fields that were easy to fund just a few years ago. And backstage sit the VCs. Under pressure to prove returns to the LPs who put money into their funds, they've been calculating "where's the safe bet right now" — and this extreme concentration is the answer they landed on.

What Actually Piled Up — In Numbers

This dataset turns on three axes. One, the money exploded but the deal count shrank. Two, 93% of that money crowded into mega-deals of ₩10B-plus. Three, a big chunk of those mega-deals were AI and robotics. Overlay those three and the phrase "selective investing" gets real. It's not that the market has no money — it's that the money won't go just anywhere.

Watch the early-stage stats especially. Normally when a market heats up, early rounds — seed and Series A — pick up first. That's the watering-the-seedlings stage. This time it went the other way. Seed-to-Series-A early deals fell 16.9% to 368. Meanwhile the average check size jumped 90.2% to ₩7.22 billion, and at the seed stage alone the average surged 175.6% to ₩3.65 billion. So even brand-new companies are getting billions of won — but only a handful of AI darlings are. The drop in early deal count itself is the scary part: it signals "back the sure things hard, and don't even look at the rest."

| Item | Detail |

|---|---|

| Source & date | THE VC, July 2, 2026 (Q2 stats) |

| H1 cumulative funding | ₩7.8005T (+204.7% YoY) |

| 2025 full-year funding | ₩6.9358T (topped in half the time) |

| H1 deal count | 540 deals (−5.4% YoY) |

| Q2 alone | 282 deals / ₩5.6271T |

| Mega-deals (₩10B+) | 141 deals (vs 85 prior, +67%) → 93.0% of all capital |

| AI/robotics investment | ₩2.685T (+485.2% YoY), 169 deals |

| Seed–Series A (early) | 368 deals (−16.9%), avg check +90.2% → ₩7.22B |

| Share of seed money to AI/robotics | 91.5% |

| Largest single deal | Dunamu secondary buy ₩2.216T (H1 ex-secondary: ₩5.5692T) |

Lay the numbers out like this and it all converges. The overall pie grew, but the overwhelming majority of that pie went to AI/deep-tech and late-stage mega-deals. Mega-deals eating 93% means, flipped around, that hundreds of sub-₩10B deals fought over the remaining 7%. This is the average trap in action. Behind the sentence "average H1 check size tripled" lurks the shadow that, for most founders, the on-the-ground reality may have gotten tougher, not easier.

Who Gets What Out of This

AI and deep-tech founders are laughing hardest. Right now, slap "AI" on it and even an early-stage company pulls in billions. With 91.5% of seed money flowing into the space, for an AI founder this is one of the easiest fundraising climates in history. Same goes for capital-hungry deep tech like semiconductors, robotics, and AI infrastructure. Fields that used to get shunned as "money pits" are now magnets for big checks.

VCs and the LPs behind them win on their own math too. As the venture market froze over the past few years, VCs took heat for "burning cash with nothing to show." Now that there's a clean theme called AI, it's far easier to tell LPs "we're betting precisely on the current of the era." A strategy of concentrating on a few mega-deals is easier to manage, and writing checks into large late-stage companies makes the exit math relatively more tractable. The big jump in Series-D-plus late-stage deals in H1 fits this exact logic.

Government and policy folks find this number handy too. "The K-startup ecosystem is back," "AI investment exploded" — those headlines dress up nicely as policy wins. But there's a trap here. A bigger total doesn't mean a healthier ecosystem. If the seedlings (early founders) are drying up while you only water the big trees, in a few years you may not have trees left to water.

To be fair, look at who clearly got frozen out too. Founders in B2C services, commerce, local, and content — anyone who can't credibly wear the AI badge — actually got squeezed harder inside the same "boom" story. The cruelest situation is money sloshing everywhere in the market except toward you. Industry chatter says B2C is "basically wiped out," and that without AI, semiconductors, or deep tech you can barely land a meeting. Behind the shiny ₩7.8T headline, non-AI founders are feeling a record funding cliff.

Past Parallels — Wins and Flops

This kind of concentration into a single theme is a pattern that recurs across venture history. On the win side, think of the early-2010s mobile boom. As smartphones spread, money crowded into the "mobile-first" theme, and the shops that bet big then produced a string of delivery, fintech, and platform unicorns. Capital concentrating during a clear technological shift isn't purely bad — genuinely huge companies get built in exactly those windows.

But there are plenty of cases where the concentration ended in a bubble. The poster child is the cheap-money liquidity party around 2021. Back then no-questions-asked money poured into content, commerce, and subscription services, and once rates rose and liquidity dried up, a lot of it ended in down rounds or shutdowns. That was when the market learned the painful lesson that "money is crowding in" does not equal "this is a good company." No one can promise today's AI concentration won't get looked back on the same way — "remember when we'd fund anything with AI in it."

One more worth flagging is the danger of early-stage funding drying up. The venture ecosystem is a pipeline business. Today's seed becomes the Series B/C of three or four years from now, which becomes the exit a few years after that. When early deal count shrinks like it is now, the pool of mid-stage companies worth funding a few years out gets thin. The US is seeing the same worry — as capital concentrates extremely into AI, the "winter for non-AI early startups" drags on — and Korea's numbers are tracing that exact path. It's a structure where a flashy total masks a hollowing pipeline, which is precisely why it deserves more caution.

How the Frozen-Out Are Countering

So do the players squeezed out of this concentration just sit still? No. They're moving in a few directions. The most common is "AI rebranding" — bolting AI features onto an existing business, or at minimum putting AI front and center in the pitch deck. Cold truth: some of these are genuine AI companies, and some are draping an AI shell on to raise money. The catch is that VCs know this too, so due diligence sorting "real AI vs. AI-washing" is getting steadily more brutal.

Non-AI founders' second move is to find entirely different funding sources. Instead of equity, they lean on revenue-based lending, government support programs, or bootstrapping to profitability. In a market where money only flows toward AI, proving you can "survive without funding" paradoxically becomes the strongest card you hold. The drop in early deals in this data partly reflects that some founders are giving up on outside fundraising altogether, or postponing it.

The VC side is splitting too. Big houses keep concentrating on late-stage AI deals, while some early-focused VCs and micro-funds are eyeing the contrarian bet: "get in cheap now on the non-AI early companies nobody's looking at, and cash in big in a few years." When everyone piles onto one side, the other side's valuations are at their most attractive. The global comparison sharpens the picture. The US and Europe are seeing the same AI capital concentration, but their absolute scale and the thickness of their late-stage deals dwarf Korea's. Korea's market is "same concentration, smaller pie," so the felt chill in the frozen-out sectors is bound to bite harder.

So What Actually Changes

For founders, this is a cold coordinate check. If you're doing AI or deep tech, this is close to the golden window for raising. Just don't forget that "money that came easy because you're AI" comes with correspondingly high expectations attached. Inflated valuations raise your down-round risk if you can't justify them in the next round. If you're a non-AI founder, the realistic read is: "stop blaming the funding market and win on revenue and survivability." The company that grinds through the dry spell is very often the one smiling in the next cycle.

For institutions and corporates (LPs and strategic investors), this number has two faces. On one hand it's a positive signal that capital is flowing into Korea's AI ecosystem; on the other, you have to watch for valuation froth building in a handful of mega-deals. Especially with early deals shrinking, the thinning pool of mid-stage companies to fund a few years out ties directly to LPs' long-term returns. You need to price in the possibility that today's flashy total comes back as a hollow pipeline in three or four years.

For the investing and policy crowd, this data is first-party evidence that Korea's venture market is starting to resemble the US in its AI concentration. Good news (total recovery) and bad news (early-stage and non-AI shut out) coexist inside a single dataset. On policy, "how do we keep the ecosystem for non-AI early founders alive" is about to become the live question. That said, this is a private company's tally, and a single mega-event like the Dunamu secondary deal can swing the whole picture — so rather than treating each figure as absolute, use it as a gauge of direction and degree of concentration. More than the ₩7.8T headline, the second sentence — 93% crowded into mega-deals — is this market's real face.

🥄 Three Things You're Probably Wondering

— So did Korea's startup market get better or worse? Both. The total clearly recovered — half a year cleared all of last year. But 93% of that money piled into AI/deep-tech and ₩10B-plus mega-deals, so for non-AI and early-stage founders it's an even colder winter. The core story is polarization: "the market's great, but I'm struggling."

— Can I take that ₩7.8T at face value? The direction's right, but be careful with the raw number. Dunamu's ₩2.216T secondary acquisition alone accounts for over a quarter of the H1 total. Strip that out and it's ₩5.5692T — still double the same period last year. So "the market did grow, but reading ₩7.8T straight as a boom is an overstatement" is the fair take.

— Is this AI concentration a bubble? Too early to call. Capital crowding in during a clear tech shift is normal, and genuinely big companies do get built in these windows. But 91.5% of seed money going to AI while early deal count shrinks does evoke the lesson from the 2021 liquidity party. How much of the pipeline survives a few years out will give the real answer.

Sources

- H1 startup funding ₩7.8T, already past all of last year — concentrated in AI (Platum)

- H1 startup funding tops all of last year, AI/deep-tech concentration deepens (Edaily)

- H1 venture funding ₩7.8T tops 2025 total; early-stage falls (Wowtale)

- Startup funding's rich-get-richer: mega-deals and AI concentration intensify (Seoul Economic Daily)

- THE VC — Korean startup investment database

Numbers and criteria are as of announcement and may change. Investment calls are yours to make!