From "where is the company" to "who owns it" — the control line just moved

In guidance issued May 31–June 1, the US Commerce Department made it explicit: licensing requirements for advanced AI chip exports apply to any business with a headquarters or parent company in China. Translation: a Chinese firm can no longer route restricted chips — Nvidia's Rubin and Blackwell, AMD's MI350x — through a subsidiary or affiliate it set up in a third country like Malaysia or Singapore. What matters isn't which country's legal entity the chip ships to, but whether that entity's ultimate owner is Chinese.

What's striking is Commerce's own admission. It framed the move as closing a loophole it had created roughly a year ago — a gap that may have let top US AI chips flow to overseas subsidiaries of Chinese AI firms for almost a year. In other words, the government conceded that "the rule existed, but it had a hole, and water leaked through it," then patched it.

Why is this big? Because the US–China semiconductor control game just got more precise. Until now, controls keyed mostly on the destination country — block chips headed to China. But companies slipped out by standing up an entity in a third country, receiving the chip there, and rerouting. This move targets that structure itself, shifting the unit of control from geography (where you are) to corporate ownership (whose you are).

The players — Commerce's BIS, Nvidia and AMD, and the gray zone called "the workaround"

Enforcement runs through the Bureau of Industry and Security (BIS) at Commerce. BIS is the core agency controlling advanced chip and equipment exports to China, and it has squeezed China's access to AI chips through the Entity List and licensing requirements. The problem: global supply chains are so complex that workarounds kept sprouting through gaps in the regulatory text. This time it went straight at the biggest of those gaps — the overseas-subsidiary route.

The companies in the crosshairs are Nvidia and AMD. Nvidia's next-gen Rubin, current Blackwell, and AMD's MI350x are the controlled chips. For these firms, China is effectively one of the world's largest AI-chip demand centers, so every tightening hits revenue directly. They have to walk a tightrope: don't break the rules, but sell as much as legally possible. As this move shrinks the "sell through a third-country entity" gray zone, the revenue variable grows again.

The key concept is the loophole. A China-headquartered firm could set up a subsidiary in Malaysia, and that Malaysian entity — "we're not China" — could buy US chips and ultimately put them to work in the Chinese parent's AI infrastructure. Looking only at the entity's location, it seemed legal; looking at the real ownership, it was a chip headed to China. Commerce closed exactly that "location vs. ownership" gap.

What's actually blocked — and what continues

The most important change is the broadened scope of the licensing requirement. Now, if a company's headquarters or parent is in China, its overseas subsidiaries and affiliates also need a US export license to receive advanced AI chips. These licenses are effectively denied, so "needs a license" is close to "can't get it." Malaysia, Singapore, the Middle East — if the entity has a Chinese parent, the same yardstick applies. The "third-country laundering" route is sealed.

It's not a blanket, indiscriminate cutoff, though. Lower-tier chips supplied under existing licenses can keep selling under current terms. It's a precision strike focused on the most powerful frontier AI accelerators, not a ban on all semiconductors. And already-shipped products stay with customers — there's no retroactive clawback. So the shock concentrates on future new supply.

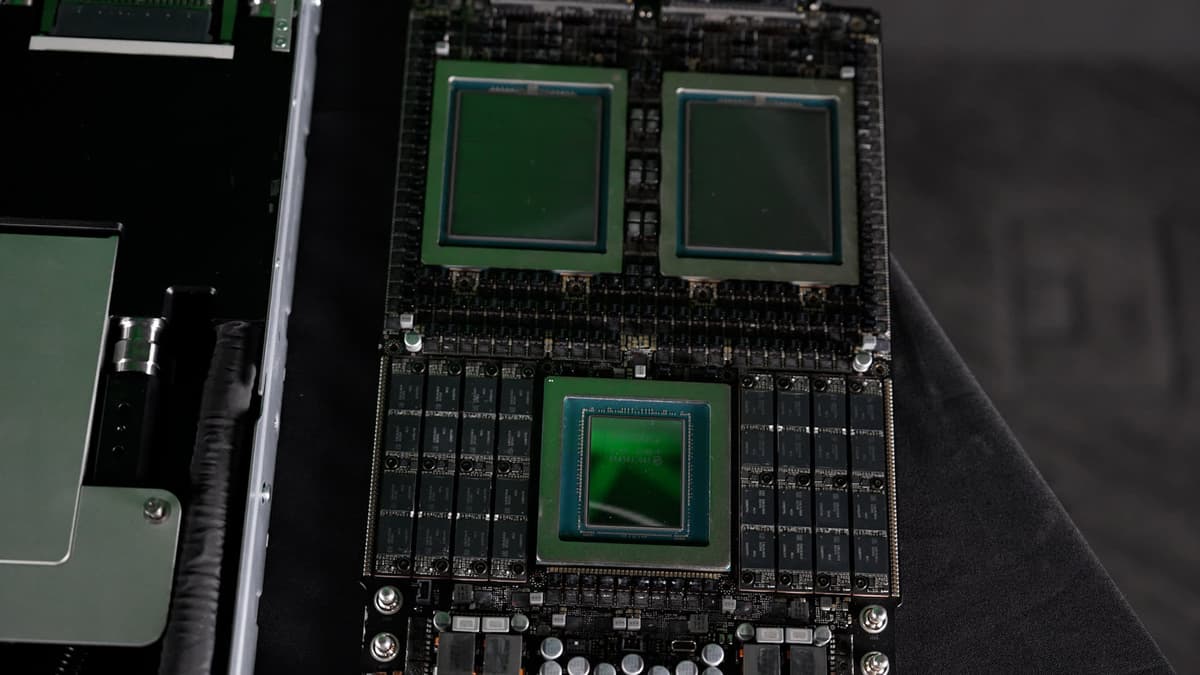

The target chips make the intent sharper. Nvidia's Rubin and Blackwell are top-tier accelerators for large-scale AI training and inference, and AMD's MI350x is a data-center chip in the same class. These are central to running frontier models — so blocking them means "slow down the pace at which China stacks top-tier AI infrastructure."

| Item | After the change | Note |

|---|---|---|

| Trigger | Applies if HQ/parent is in China | Ownership-based |

| Blocked path | Workaround buying via overseas subsidiary | "Third-country laundering" sealed |

| Target chips | Nvidia Rubin/Blackwell, AMD MI350x | Top-tier accelerators |

| Still allowed | Lower-tier chips under existing licenses | Precision strike |

| Already shipped | Stays with customer | No retroactive clawback |

Who gains, who loses — the US, Nvidia, China

For the US government, it raised the effectiveness of its controls. However strong a rule is, an open workaround makes it useless. This move closes the biggest hole — China stacking top-tier chips through overseas entities. Read alongside the same period's "frontier-model early-access EO," the picture sharpens: the US is now treating AI as a national-security asset on both hardware and software fronts.

For Nvidia and AMD, it's a near-term negative. As the third-country sales route shrinks, the revenue variable widens. But the caveat — "lower-tier chips under existing licenses keep selling" — means the blow isn't total. These firms have already adapted by building "control-compliant chips" with downgraded specs; they'll keep walking that tightrope. The catch is that China-bound revenue uncertainty has spiked again.

For China, the pressure ratcheted up a notch — getting top-tier US chips, legally or via workarounds, just got harder. But that's also fuel and pressure to build up its own chip industry. Expect demand to shift toward domestic AI chip makers like Huawei and Cambricon, and a stronger national drive to "reduce dependence on the US." Controls are effective short term, but long term they're a double-edged sword that pushes the rival toward self-sufficiency.

Echoes from history — patching holes, again, with mixed results

The history of export controls is an endless loop: rule → workaround discovered → patch the hole → new workaround. The results always cut both ways.

Where it worked — step-by-step tightening. Since 2022 the US has squeezed advanced-chip controls on China repeatedly. It first blocked by spec (compute, bandwidth); when Nvidia shipped a slightly downgraded "control-dodging chip" (think the H20 tier), the controls chased that chip too. This "parent-company nationality" test follows the same pattern — when a workaround appears, abstract the criterion one level higher to catch it. The control authority keeps learning the market's evasive moves and tightening the net.

Where it falls short — smuggling and gray markets. Conversely, controls have never been airtight. However tight the rule, a certain volume of chips leaks through third-country brokers, gray markets, and smuggling routes — that's the repeated reality. Sealing the "overseas subsidiary" route will spawn new, smaller-scale workarounds: resale in tinier lots, disguised imports. So read this as "patch the biggest hole and sharply raise the cost of evasion," not "total blockade."

The contrast — controls breed self-sufficiency. Historically, strong export controls also accelerate the target's domestic substitution. As many tech sanctions since the 1980s showed, short-term blockades push rivals toward independent ecosystems over the long run. China's AI-chip self-sufficiency could speed up as an unintended consequence of US controls — the fundamental dilemma baked into this move.

How rivals counter — China, third countries, and the chip makers

China's first card is "accelerate localization" — ramping volume and performance of domestic AI chips like Huawei Ascend and Cambricon to cut US dependence. Its second is "develop new workarounds" — restructuring ownership in more complex ways or inserting third-country partners to dodge the parent-nationality test. The cat-and-mouse of control and evasion simply moves to the next round.

Third countries like Malaysia and Singapore are now in a bind. They've traded with both the US and China as hubs for chip assembly, testing, and data centers — and now America's gaze on "locally incorporated entities with Chinese parents" has sharpened. To protect their own industries without violating US controls, they'll have to adopt tougher customer due diligence (KYC) and end-user verification. The "way stations" of global chip distribution are inheriting the regulatory burden.

Nvidia and AMD will continue the adaptation they've already practiced — building "control-compliant chips" tuned to the rules, and shifting weight toward non-China demand (the Middle East, Southeast Asia) within legal bounds. They'll aim for a delicate balance: lower China revenue dependence without fully abandoning it. But as controls tighten, the maneuvering room for "compliant chips" narrows too, raising long-term pressure to model the China business conservatively.

So what actually changes — by persona

If you're in semiconductors or hardware, the key is that the unit of control shifted to ownership. Going forward, who a customer's ultimate owner is (parent nationality) becomes the variable that decides whether a deal is allowed. If you touch supply chains or distribution, prepare much stricter customer due diligence and end-user verification. We've moved to an era that scrutinizes "whose is it" as much as "where does it ship."

If you use AI infrastructure as a company or developer, the direct impact is limited for now, but the macro trend is worth knowing. As US–China chip controls intensify, global GPU supply splits more along geopolitical lines, and regional availability and pricing can diverge. If you depend on infrastructure in a specific region, keep supply diversification and alternative accelerators (domestic chips, clouds) in view.

If you're an investor or policy watcher, this move signals that the "AI = national security" frame has descended to the hardware layer. Read with the same week's frontier-model EO, it's clear: US AI strategy is being securitized on both the model and chip fronts simultaneously. Watch two threads together — near-term China-revenue uncertainty for US chip makers, and long-term acceleration of Chinese chip self-sufficiency. Controls are effective, but they're also the seed that grows a rival's independent ecosystem.

References

- Al Jazeera (Reuters-sourced) — US says ban on AI chip shipments applies to Chinese firms outside China

- U.S. takes step to halt Nvidia AI chip shipments to Chinese firms outside China — CNBC

- [News] U.S. Moves to Block AI Chip Exports to Overseas Chinese Units — TrendForce

- Bureau of Industry and Security (BIS) — U.S. Department of Commerce

- Nvidia — Data Center GPUs