Second Fintech Acquisition in Six Months

OpenAI bought another fintech company.

On April 13, OpenAI confirmed the acquisition of personal finance AI startup Hiro Finance. Terms weren't disclosed. All ten Hiro employees are joining OpenAI. The Hiro consumer service shuts down April 20, with all user data permanently deleted by May 13. Industry insiders describe the deal as a strategic "acqui-hire" — a talent acquisition wrapped in acquisition paperwork.

The timing matters more than the deal itself. In October 2025, OpenAI acquired Roi, another personal finance app. Two acquisitions in the same vertical within six months isn't opportunism — it's strategy with a clear target.

For a company tracking toward $20B+ in annual revenue, methodically scooping up ten-person startups is a signal about what OpenAI actually values right now: not technology, but operators who've already shipped consumer products in a specific domain.

Acquirer Profile — OpenAI's Recent M&A Cadence

OpenAI has been on an M&A sprint since late 2024.

The pattern isn't big splashy deals. It's rapid absorption of sub-10-person startups through acqui-hires: Context.ai, Crossing Minds, Alex, Roi, and now Hiro. The common thread: every target built a consumer-facing AI product in a specific vertical. OpenAI isn't buying technology — it's buying founders who've already wrestled with a domain problem end-to-end.

OpenAI has done bigger deals too: $6.5B for Jony Ive's io hardware venture, $2.4B for Windsurf's core team and licensing. But the far more frequent pattern is vertical acqui-hires. More than five publicly reported acqui-hires landed in 2025 alone.

| Date | Target | Structure | Focus |

|---|---|---|---|

| Jun 2024 | Rockset | Acquisition | Database, inference infra |

| Jun 2024 | Multi | Acqui-hire | Collaboration tools |

| May 2025 | io (Jony Ive) | Acquisition $6.5B | AI hardware |

| Jul 2025 | Windsurf team | License + talent $2.4B | Coding agents |

| Oct 2025 | Roi | Acqui-hire | Personal finance |

| Apr 2026 | Hiro Finance | Acqui-hire | Personal finance |

Two consecutive acqui-hires in personal finance is not a coincidence. It means "consumer financial AI" has a seat at the internal priority table at OpenAI.

Target — What Hiro Finance Actually Was

Hiro's core concept was a "Personal AI CFO."

Users entered their salary, debts, monthly expenses, and savings goals. The AI generated multiple financial scenarios and explained the results in plain English. "If I increase my rent by $300/month, how does that affect my savings in three years?" Hiro answered with specific numbers and projections. Founder Ethan Bloch spent nearly two years stitching together various models — including OpenAI's GPT family — to get the reasoning to the point where he'd trust it with his own money.

One design choice stands out. Hiro shipped a verification feature that let users check the accuracy of the AI's math step by step. At a time when LLMs are notoriously unreliable at numerical reasoning, Hiro leaned into transparency rather than hiding the problem. In a domain where wrong answers create real financial harm, that design philosophy is a moat.

| Detail | Info |

|---|---|

| Founded | 2023 |

| Flagship launch | Late 2025 (about 5 months before acquisition) |

| Team size | About 10 (all joining OpenAI) |

| Total funding | Not publicly disclosed (seed / early stage) |

| Lead investor | Ribbit Capital |

| Co-investors | General Catalyst, Restive |

| Founder | Ethan Bloch — serial fintech founder |

| Prior exit | Digit (founded 2013, sold to Oportun in 2021 for $200M+) |

| Service shutdown | April 20, 2026 |

| Data deletion complete | May 13, 2026 |

The founder's track record explains the deal's real value. Ethan Bloch built Digit — an automatic savings service — and ran it for eight years before selling to Oportun in 2021 for over $200 million. He has actually operated a personal finance product at scale. OpenAI isn't buying Hiro's code; it's buying the muscle memory of someone who's already done this.

Source: commons.wikimedia.org · Public domain (below threshold of originality)

Source: commons.wikimedia.org · Public domain (below threshold of originality)

Deal Structure — The Acqui-hire Template

The deal follows the standard acqui-hire playbook.

First, no numbers. TechCrunch, PYMNTS, American Banker, and FintechFutures all reported "terms were not disclosed." Given that Hiro raised at seed level and the flagship product shipped only five months ago, the headline number is probably modest — mostly covering investor principal plus retention bonuses for the team. Typical range for this structure: $50M to $200M.

Second, payment is likely equity-weighted. OpenAI's standard offer package includes Profit Participation Units (PPUs) or RSUs. As the key retention target, founder Ethan Bloch almost certainly signed a four-year vesting schedule with milestone-based bonuses.

Third, the product dies immediately. The acquisition was announced April 13, and the service shuts down April 20 — a single week of runway. All user data gets deleted by May 13. This tells you clearly that OpenAI has zero intention of keeping Hiro's app alive. They want the team, not the product.

Regulatory risk didn't materially affect the close. Hiro operated as a personal finance tool (advice), not a regulated financial service, so no bank license or SEC investment adviser registration was involved. That said, the moment OpenAI integrates this team's work into ChatGPT's consumer flow, new regulatory surfaces open up — potentially SEC, CFPB (Consumer Financial Protection Bureau), and state-level consumer advice rules.

Why This Company, Why Now

OpenAI's public language emphasizes "personalization and life management."

The official rationale is credible. ChatGPT has already become a daily tool for people asking personal finance questions: canceling subscriptions, setting budgets, making investment calls, evaluating insurance. But ChatGPT's answers have been generic — it doesn't know your actual accounts, actual spending, actual goals. Hiro's team spent two years figuring out how to structure that kind of data for an LLM to reason over.

The industry read is more specific. The same week Hiro closed, Revolut published PRAGMA — a foundation model trained on 40 billion financial events. Anthropic's Claude is running live experiments with agent capabilities that call external services. Visa announced an AI agent payment system earlier this month. Fintech and AI are converging on a single point, and OpenAI is sending a "we have finance people now" signal right into that convergence.

Two fintech acquisitions signal that the future of AI assistants is shifting from "conversation" to "execution." Not an AI that just talks about your money — an AI that actually manages it.

Source: commons.wikimedia.org · CC BY-SA 4.0

Source: commons.wikimedia.org · CC BY-SA 4.0

Integration Risk — Lessons from Similar Acqui-hires

For acqui-hires, the 18–24 months after close is where value is made or lost.

History shows a split. When Google acquired DeepMind for approximately $500M in 2014, they kept the research team in London with guaranteed independence — and the bet paid off over a decade. When Facebook acquired Instagram in 2012, independence eroded over time, and both founders (Kevin Systrom and Mike Krieger) walked away in 2018. If an acqui-hire is really about the people, the deal has no lasting value once those people leave.

OpenAI's own recent pattern gives us reference points. In the Roi deal, only the CEO (Sujith Vishwajith) joined OpenAI — the other three team members did not. That's a "founder-only" acqui-hire pattern aimed at a specific leader. Hiro is structurally different: all ten join. OpenAI is lifting an entire functional team into a single "financial AI" workstream, not just grabbing a founder.

Three integration risks stand out. First, can a repeat founder like Ethan Bloch adapt to big-company bureaucracy after eight years running his own CEO seat at Digit? The classic startup founder exhaustion loop often produces a one-year tenure. Second, will a team that just shut down its own product retain the motivation to rebuild something inside OpenAI? Third, as financial regulation matures through late 2026, will OpenAI's compliance organization scale fast enough to back this team properly?

Sector Consolidation — The AI Fintech Map

OpenAI isn't alone. The intersection of AI and finance has turned into one of the hottest battlegrounds of 2026.

Revolut shipped PRAGMA, a foundation model trained on 40 billion financial events. Klarna is already serving an OpenAI-powered shopping assistant to over 10 million users. Korean fintechs Toss and KakaoPay accelerated their own LLM fine-tuning efforts from early 2026. Visa and Mastercard each announced AI-agent payment protocols — changes that redesign the card network layer itself.

| Player | 2026 Fintech AI Move | Approach |

|---|---|---|

| OpenAI | Hiro + Roi acqui-hires, ChatGPT finance integration pending | Team acquisition → internal build |

| Revolut | PRAGMA foundation model, AIR assistant launch | Train own model |

| Anthropic | Claude agents + external service orchestration | Agent protocol |

| Visa | AI agent payment system | Network-level |

| Mastercard | Agent Pay protocol | Network-level |

| Klarna | GPT-based shopping assistant, 10M users | External API dependency |

| Google (Gemini) | Google Wallet + Gemini integration | Extend existing platform |

OpenAI's position in this map is unusual. It has no payment network (Visa/Mastercard) and no installed user financial data (Revolut/Klarna). Instead it wields ChatGPT's 500M+ monthly users as a distribution weapon and builds the financial layer directly on top of that consumer touchpoint.

What This Means for You

For consumers, changes will likely be visible in 6–12 months.

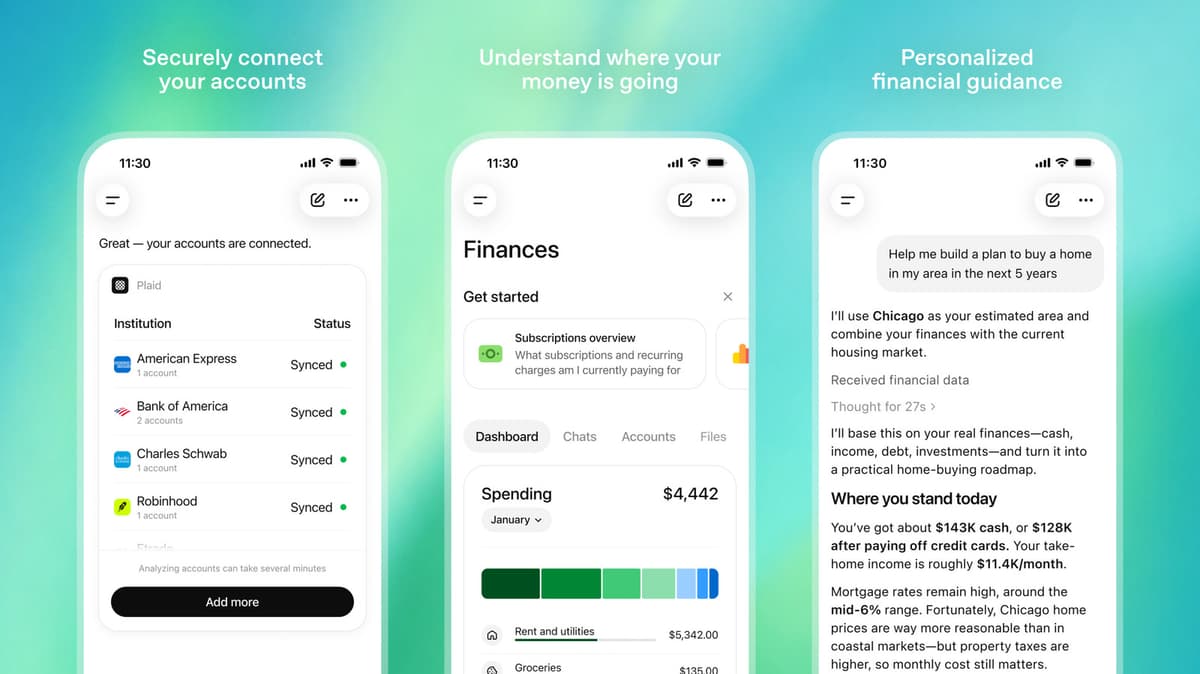

The most plausible rollout: ChatGPT's "Projects" or "Work with Apps" surface gains financial connectors. Through something like Plaid's bank-linking APIs, ChatGPT reads your accounts and uses the scenario-simulation playbook Hiro refined to answer with actual numbers. "Analyze my spending this month." "Calculate whether this investment makes sense." ChatGPT replies with numbers and reasoning. This democratizes financial advice that currently runs hundreds of dollars per session — especially valuable for people who've been priced out of professional financial planning entirely.

The regulatory counterweight follows. SEC investment advisory rules, CFPB consumer finance-advice scrutiny, state-level fiduciary standards — all come into play. Hiro's decision to include a math-verification feature wasn't just UX; it was defensive design for exactly this world. Once liability attaches to OpenAI directly, product decisions will get more conservative fast.

For developers, the signal is unambiguous. OpenAI is expanding into vertical domains — finance, health, education — through team acquisitions. If you're building in one of these verticals, two options remain. Either move fast enough to own distribution before OpenAI lands. Or go deeper on domain expertise, building on top of OpenAI's platform in a way they can't replicate with a ten-person team.

References

- TechCrunch: OpenAI has bought AI personal finance startup Hiro

- American Banker: OpenAI acquires personal finance startup Hiro

- The Decoder: OpenAI acquires AI finance startup Hiro, which built a personal AI CFO

- PYMNTS: OpenAI Buys Personal Finance Platform Hiro

- TechCrunch: OpenAI is doubling down on personalized consumer AI (Roi acquisition, Oct 2025)

- FintechFutures: OpenAI snaps up AI personal finance start-up Hiro

{kind=link}

{kind=link}