$3.2 billion to plant the optical-fiber supply chain on US soil — May 6

Here's the deal. On May 6, Nvidia and Corning announced two things at once. First, Nvidia secured the right to invest up to $3.2 billion in Corning equity through a $500 million pre-funded warrant. Second, Corning committed to three new optical-only fabs in North Carolina and Texas, generating 3,000+ jobs. The headline number: a 10x increase in US optical manufacturing capacity.

After the announcement, Corning rallied 12% and Nvidia 6%. On May 7 Jensen Huang told CNBC the deal will "revitalize American manufacturing" — landing right in the Trump administration's "Made in America" framing.

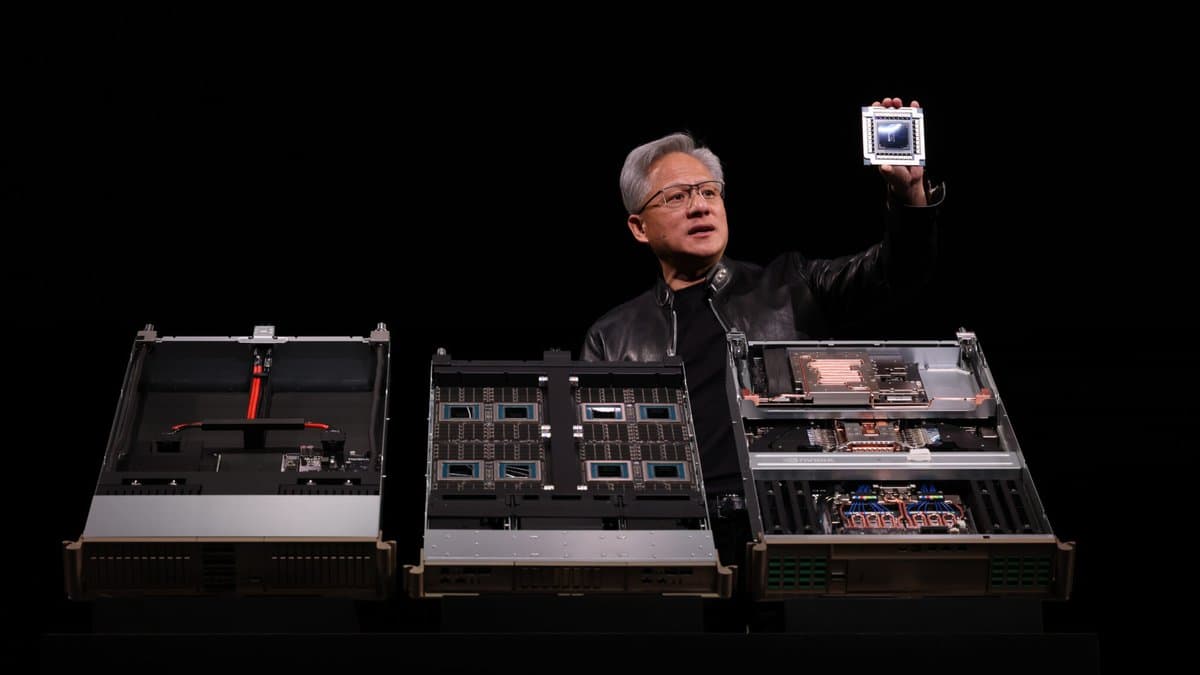

Why this isn't just capital partnership: Nvidia is locking the invisible bottleneck of AI data centers — optical fiber + optical interconnect — with capital. As GB300 and Rubin generations push NVLink 5/6 past copper-cable limits, co-packaged optics (CPO) and optical backplanes become standard. Optical fiber, ferrules, lenses, connectors, MPO components — Corning is central to all of them. Nvidia isn't just making the GPU. It's also tying down the "thread" that connects the neural net of GPUs.

Each player — Nvidia, Corning, deal structure

Nvidia. In the first four months of 2026, Nvidia committed over $40 billion in AI equity bets (OpenAI $30B, Corning $3.2B, IREN $2.1B, Intel $5B). Part of a "vendor financing" strategy that turns GPU demand into capital. The Corning case differs: capital flows into a supplier, not a customer like OpenAI or IREN. So this isn't a bet to manufacture GPU revenue; it's a bet to guarantee the component capacity that makes GPU shipment possible.

Corning. Founded 1851, ~$70B market cap (post-announcement). Global #1 in optical fiber, Gorilla Glass and automotive display glass. AI infrastructure exposure across (1) data center optical fiber cabling (external interconnect), (2) co-packaged optics ferrules / lenses (inside the GPU package), (3) optical backplanes (inside server racks). All three growing double digits QoQ. The $3.2B will fund NC/TX fab capacity ramp + R&D + hiring.

Deal structure. Two tranches: (1) $500M pre-funded warrant: Nvidia pays $500M now, gets the right to exercise Corning shares later. (2) An additional $2.7B securities purchase agreement that releases capital in stages tied to fab ramp. Total $3.2B is ~4.5% of Corning's market cap. Nvidia starts with non-voting option positions and converts to common stock in stages.

New fab locations. 1 in NC (Hickory, expanding existing campus), 2 in TX (greenfield). All optical-only. Targeted online: H2 2027. Of 3,000+ jobs: ~30% engineering/R&D, 60% manufacturing, 10% management/support.

Core developments — why optical fiber is the AI infrastructure choke point

AI data center performance is set by three axes: GPU compute + memory bandwidth + interconnect. Frontier models like GPT-5, Gemini 3.1, Claude Opus 4.7 train on 10K–100K GPU clusters per model. If the interconnect between GPUs is slow, compute idles. That's why NVLink 5/6 + Spectrum-X + InfiniBand 800G are central technologies.

| Layer | Legacy (copper) | New (optical) | Corning role |

|---|---|---|---|

| Rack-to-rack | DAC ~5m max | Optical fiber 50–300m | Fiber cabling |

| Server-to-switch | 25–100G | 800G–1.6T | MPO connectors / ferrules |

| Inside GPU package | Copper traces | Co-packaged optics | Ferrules, lenses, waveguides |

| Backplane | Copper PCB | Optical backplane | Embedded optical modules |

| Date | Event |

|---|---|

| 2026-05-06 | Nvidia–Corning $3.2B partnership announced |

| 2026-05-07 | Jensen Huang on CNBC: "revitalize American manufacturing" |

| 2026-05-08 | Corning +18% (cumulative two-day), Nvidia +6% |

| 2027 H2 | NC/TX new fabs targeted online |

Corning's alternatives: Japan's Fujikura, Sumitomo Electric Industries, Korea's LS Cable & System, China's Yangtze Optical Fibre. But: (1) Corning has IP advantage in advanced optical ferrules like CPO, (2) US "Made in America" policy makes domestic supply chain a political priority, (3) Nvidia capital gives Corning a lead-time edge over rival vendors. So Nvidia GPU shipment ramp directly depends on Corning capacity.

Who wins — beneficiary breakdown

Nvidia gets shorter GPU lead times. Optical interconnect component shortages were delaying GB300 ramp by 7–10 weeks. With Corning capacity multiplied 10x, that bottleneck dissolves. Plus, the capital appreciates as Corning's market cap rises — the $500M warrant has already gained 18% in paper value.

Corning gets revenue and margin lift. Optical segment revenue could double from ~$9B in 2025 to ~$18B by 2028. Operating margin expands from 16% to 22%. Nvidia capital cuts Corning's own capex burden by half — improved P&L efficiency.

Broadcom and Marvell ride along. Optical interconnect SerDes / DSP / transceiver chips pair with Corning fiber. As Corning capacity grows, optical SerDes demand rises. Broadcom AI revenue's $30B 2026 visibility gains support.

NC and TX local economies: Of 3,000+ new jobs, assuming engineer ~$120K, manufacturing ~$70K, management ~$90K average salaries, direct wages ~$250M/year. Indirect economic effects (housing, services, education) add another $500–700M/year. Reason both states actively welcome the deal.

US government (Trump 2.0): Symbolic success of "Made in America" AI infrastructure policy. Likely partial CHIPS Act + AI infrastructure subsidy flow into the new Corning fabs. Political capital secured. Reduced China/Taiwan supply dependency for optical manufacturing addresses national security concerns.

Pressured: Japan's Fujikura/Sumitomo, Korea's LS Cable, China's Yangtze Optical Fibre. US optical fiber market share consolidates to Corning. LS Cable may pivot to Southeast Asia / India data centers. Japan responds via Fujikura's domestic capacity expansion under government optical subsidies.

Past parallels — Cisco-fiber 1999, TSMC-semis 2020s, Intel IDM 2.0

Cisco-fiber, 1999. During the internet infrastructure boom, Cisco capitalized fiber suppliers to guarantee router demand. Result: Cisco market cap parabolic, then -80% in dot-com bust. Difference: Cisco 1999 revenue was 100% customer-capex dependent; Nvidia GPU demand is diversified across data center + consumer. Corning isn't a 1999-style fiber bubble vendor — it's a 130-year industrial company with solid fundamentals. Still, the same risk persists: if optical interconnect capacity outruns demand, price competition emerges.

TSMC US onshoring, 2020s. Arizona fab 4nm/2nm production. US government subsidies + own capex secure domestic supply. But labor / process costs run 50%+ higher than Japan/Taiwan, pressuring margins. Corning's NC/TX fabs face the same structural cost pressure. How much of that Nvidia capital + government subsidies cover will determine ROI.

Intel IDM 2.0 (2021–2024). Bundled foundry + chip design + packaging into a full stack with $100B+ capex. Margin stagnation drove a steep market cap decline. Lesson: vertical integration full-stack is determined by capex efficiency and cycle management. Nvidia's Corning bet is narrower — guaranteeing critical component capacity rather than full-stack integration — so risk is lower than the Intel case. But if optical interconnect standards shift quickly, the new Corning fabs could become obsolete.

Counter-case: Meta-Reality Labs. Bundling own R&D + own distribution into a full-stack bet led to a 70% market cap derating. Nvidia's Corning bet has clear direct revenue contribution (faster GPU shipment ramp), so the same pattern is unlikely. But if the optical interconnect market itself stagnates, capital efficiency could come into question.

Competitor counterplays — TSMC, Broadcom, Japanese fiber, China's Yangtze

TSMC's counter. Accelerated in-house optical packaging (SoIC + CoWoS-L). On May 9 TSMC announced an optical transceiver collaboration with Japan's Sumitomo. Direct counter to the Nvidia-Corning alliance.

Broadcom's counter. As #1 in optical SerDes + DSP, a natural partner to Corning fiber. But also Alphabet TPU design partner — keeping a non-Nvidia full-stack option in parallel. "GPU dependency diversification" will be the next-quarter messaging.

Japan's Fujikura / Sumitomo. Domestic capacity expansion via NEDO subsidies. Strong in Japan + Southeast Asia data centers. US market entry is blocked by the Nvidia-Corning alliance.

Korea's LS Cable & System. #4 globally. <5% US market share. Counter: (1) prioritize Southeast Asia, India, Middle East data centers, (2) defend Korean data centers (Naver, Kakao, KT, SKT), (3) avoid head-on competition with Corning via differentiated products like next-gen ribbon fiber and micro duct.

China's Yangtze Optical Fibre / Hengtong. Strong in domestic + Belt-and-Road data centers. Practically blocked from US entry. Counter: ride Chinese government AI infrastructure subsidies + the domestic GPU (Huawei Ascend) ecosystem.

So what changes — by persona

Data center operators: Optical interconnect lead times shrink, accelerating GPU cluster ramp. But Corning pricing dependency rises — weakened negotiation leverage. Multi-vendor sourcing (Corning + Fujikura + LS Cable) is recommended.

Korean cable / fiber companies (LS Cable, Daehan Optical Communications): US domestic market is closed off. Survival cards: prioritize emerging markets (India NaviStack, Indonesia NeutraDC, UAE G42) + accelerate next-gen optical R&D (high-density ribbon, hollow-core fiber).

Investors: Corning $70B → $120B scenario by 2027. Nvidia warrant capital appreciation rides along. Consider increased weighting in optical interconnect ETFs / semiconductor packaging ETFs. Caveat: derating risk if optical interconnect market growth stalls.

US policy analysts: First major success of "Made in America" AI infrastructure policy. CHIPS Act + AI infrastructure subsidies likely extend to gas/tank/optical fiber/HBM domestic capacity. Korean and Japanese component suppliers face increasing pressure to build US fabs.

Engineers / supply chain managers: Need familiarity with optical interconnect standards (NVIDIA OSFP, OIF, IEEE 802.3 800GE). Co-Packaged Optics (CPO) likely becomes industry standard 2027–2028. Optical transceiver / external optical module market gradually absorbed by CPO.

References

- NVIDIA and Corning Announce Long-Term Partnership — NVIDIA Newsroom, 2026-05-06

- Nvidia to invest up to $3.2 billion in Corning — CNBC, 2026-05-06

- Nvidia Inks $500 Million Deal With Fiber-Optic Maker Corning — Bloomberg, 2026-05-06

- Co-packaged optics roadmap — OIF, 2026

- NVIDIA Spectrum-X / NVLink 6 — NVIDIA Developer

- Corning Q1 2026 earnings (optical communications) — Corning IR

Key signals to track over the next 12 months

Four signals will determine whether the Nvidia-Corning bet pays off as planned or stalls under execution risk. First, NC Hickory campus break-ground date — every quarter of permit delay translates into 3–4 weeks of GPU shipment delay through 2027. Second, Co-Packaged Optics adoption rate at GB300/Rubin tier — if CPO penetration crosses 30% by year-end 2026, Corning's optical revenue trajectory accelerates by another 30%; if stuck below 15%, the $3.2B bet underperforms. Third, the response from Fujikura/Sumitomo/LS Cable — coordinated US fab announcements in next 6 months would signal a defensive industry consolidation, while no response cedes the US market to Corning. Fourth, ERCOT power capacity for Texas optical fabs — Texas is already grid-strained from data center demand, and the new Corning fabs add 100–200MW of industrial load that needs PPA negotiation. Track these four — they collectively decide whether the optical bottleneck stays unblocked through the AI capex super-cycle.

Bottom line

This isn't just a supplier deal — it's Nvidia's third-quarter capital-cycle move locking the invisible bottleneck of AI infrastructure. The bet sets up a 2027–2030 cadence in which GPU shipments scale because the optical fiber to connect them is finally guaranteed. The capital efficiency question — does $3.2B return as $10B+ in unlocked GPU revenue — answers itself in 24 months. Watch Sweetwater Texas, Hickory NC, and Corning's Q1 2027 optical segment disclosure for early proof.